RRSPs for Canadian Business Owners, should you invest?

NOTE: This article references the proposed 2024 Federal Budget increase on the Capital Gains Inclusion Rate from 1/2 to 2/3. This proposal never received Royal Ascent and was officially scrapped in 2025.

As a small business owner, your corporation might generate more income than what you need for daily operations or personal expenses. What you do with this surplus income is crucial for your financial future.

You have two main options:

- keep the funds inside the corporation

- withdraw, pay income tax and invest personally

Today we’re going to go through these 2 scenarios – do you take your money out of the corporation and invest in your RRSP or do you keep it in the corporation and invest there?

Let’s get into it….

The main research and numbers that I’ll use in this video are from a really good Sun Life article - RRSPs and TFSAs for Small Business Owners (PDF)

The article is about RRSPs and the benefit to Canadian business owners.

The TL;DR is that for a lot of business owners, maximizing contributions to your RRSP is a smart strategy, especially over a long-term time horizon.

This approach got even better with the 2024 Federal Budget changes including the capital gains inclusion rate increases introduced in June.

Basically the new 2024 Federal Budget changes made RRSPs more valuable as a tax-efficient savings vehicle.

Understanding Corporate vs. Personal Tax Strategies

Many small businesses in Canada benefit from low tax rates on active business income, known as the “general rate.” Across the provinces, the combined federal and provincial/territorial general tax rate ranges between 23% to 31%. Then if you are a small business, you get the small business deduction which further reduces tax rates on your first $500,000 of net active business income. Across the different provinces, this ranges from 9% to 12.20% on your first $500k in net income.

Contrast this to your personal tax rate which is often higher than your corporate active business income tax rates.

In 2024, the highest combined marginal personal tax rates average 50% across Canada for regular income. Dividend income is taxed at lower rates, because of the corporate tax that you already paid:

In Canada, eligible dividends get taxed between 28% - 46% when you pay the general business rate, you pay 37% - 49% for non-eligible dividends when your corporation pays the small business rate. When you first look at it, the lower corporate tax rates suggest a potential tax deferral advantage by keeping funds inside your corporation. But this advantage depends on several factors.

For instance, RRSPs may initially allow for more invested capital compared to corporate investing. Still, the ultimate outcome depends on after-tax income when you withdraw the funds to use for yourself personally.

The Key Factors to Consider for Tax Optimization are…

- Your corporation’s initial tax rate (do you pay the general rate or the small business rate).

- Whether your tax bracket changes between the time when you invest and when you withdraw

- The type of investment income generated – for example, do you make interest income, dividends, capital gains, or deferred gains in your investment?

- The time horizon for your investment. When do you need the money and what’s it for?

These are important factors to consider as a small business owner so that you can make the best-informed decision to maximize after-tax returns and achieve your long-term financial goals.

RRSP vs. Corporate Investing

When it comes to investing surplus income as a small business owner in Canada, you have the option putting money into your RRSP or keeping the money in your corporation or Holdco.

Each way, whether you do RRSP or keep the money in your corp, has unique tax implications that can significantly impact your after-tax income, and you need to know about them.

Tax Prior to Investing: Corporate vs. RRSP Contributions

For RRSP contributions, taxes are deferred, and it lets your corp deduct contributions paid as salary, effectively reducing your taxable income when you put money into an RRSP.

In contrast, if you keep the money in your corp, you’ll get hit with corporate tax on business income, which is at either the general tax rate or the small business tax rate, depending on your total corporate income.This upfront tax treatment varies depending on whether you invest personally through an RRSP or keep the money in your corporation.

Tax on Growth While Invested

This is super important – the tax treatment of growth while invested is significantly different between RRSPs and investing in your corporation. Investments in your RRSP get tax-deferred growth, meaning you won’t pay taxes on gains until you withdraw the money. In your corporation, however, different types of investment income get different tax rates. Interest income is taxed between 46.67% and 54.67% depending on your province.

Dividends from Canadian companies are taxed at 38.33% and capital gains count as passive income and are taxed at 50% of whatever your corporate rate is. Now there’s been some changes to how capital gains are taxed with the new rules from the 2024 Federal Budget. Capital gains made after June 25, 2024, are now taxed with the higher capital gains inclusion rates of 31% - 36% depending on your province.

Notably, corporations also get credits like the refundable dividend tax on hand RDTOH. Which allows tax credits when dividends are distributed to shareholders.

So, we've talked about 3 big things so far

- Understanding Corporate vs. Personal Tax Strategies

- Upfront tax deductions in your RRSP vs no deduction when investing in the corporation

- How the investment gets taxed or not taxed as it grows corporately vs in your RRSP

Basically, what happens when you put the money into the investment and what happens from a tax perspective while you’re growing it. Now we'll talk about what happens later when you want to take it out and use it and live your life. And later about comparing performance between the 2 options of putting your money into an RRSP vs keeping it in the corporation and if your business is paying the general rate or the small business rate.

Taxation Inside the Investment Vehicle Upon Disposition

When investments are withdrawn or liquidated from your RRSP, the funds are fully taxable as ordinary income. Conversely, within a corporation, capital gains are treated as passive income, and you pay tax when you liquidate or rebalance the investment.

Personal Tax on Removal

For RRSPs, withdrawals are fully taxable as ordinary income whenever you take it out. Corporate-held investments are more flexible because your corp can can distribute investment income to shareholders in different forms.

This includes tax-free capital dividends credited to the Capital Dividend Account (CDA), as well as eligible and non-eligible dividends.These dividends are grossed up and taxed accordingly, with personal tax rates at 15% for non-eligible dividends and 38% for eligible dividends.Dividends provide an opportunity to recover previously paid RDTOH.

Contribution and Age Limits for RRSPs and Corporate Investments

One of the downsides of RRSPs is that RRSPs have annual and cumulative contribution limits and age restrictions. In 2024, the contribution cap is 18% of earned income, up to a maximum of $31,560. But your contribution limit will depend on how much you’ve built up over the years. You can check your available contribution limit on your My CRA account on the left side when you login.

Additionally, RRSP accounts have to convert to an income stream by the end of the year in which you turn 71 regardless of if you want to take out the money or not. We actually have a few clients like this – where they are doing very well now and don’t need the money in their RRSP and now they’re forced to take it out and pay 50% in taxes. The benefit of investing corporately is you don’t have set contribution limits or age limits, so this gives you greater flexibility for long-term investments.

The choice between RRSPs and corporate investing ultimately depends on a lot of things, but a lot of people think about the potential for tax deferral and the after-tax income when you want to use the money.

Factors like initial tax rates on active business income if you’re paying the general rate or the small business rate, changes in personal tax brackets over time, the type of investment income you’re earning, and the investment duration all play a role when figuring out your optimal to getting the maximum after-tax income from your investments.

Let’s Compare Performance between the Small Business Tax Rates – if you’re paying the General Rate or if you’re Paying the Small Business Rate

Sun Life uses a guy named Andre to illustrate and analyze a situation like in the TFSA article, which you can read here: https://advisorhub.sunlife.ca/content/dam/sunlife/regional/canada/documents/slfd/rrsps-for-business-owners-en.pdf

So, Andre lives in Ontario and earns an income of $300,000 paid as a salary. This puts Andre in the highest tax bracket. His corporation, which is also in Ontario, has an extra $10,000 pre-tax surplus at the end of the year.

If Andre’s corporation pays him an additional salary, it can deduct the $10,000 from its pre-tax profits, reducing the corporate income to zero. Andre then receives the full $10,000, which he can contribute entirely to his RRSP. This approach results in a $10,000 RRSP investment.

Andre also won’t pay any tax on this money right now because the RRSP deposit is deductible against his personal taxable income on the $300,000 salary. The other way, if Andre keeps the extra $10,000 in the corporation, the after-tax amount available for investment depends on the corporation’s tax rate:

At the Small Business Rate of 12.2%, the corporation pays $1,220 in taxes, leaving $8,780 to invest.

If Andre’s company pays the General Rate tax at 26.5%, the corporation pays $2,650 in taxes and has $7,350 left to invest.

So, if he invests personally into his RRSP he starts with the full $10,000 to invest:

- If his corporation pays general rate tax, then his corporation starts with $7,350 to invest

- And if the corporation pays the small business rate then it starts with $8,780 to invest

The corporation would then invest this after-tax amount, subject to corporate passive investment tax rates. Notably, changes in the 2024 Federal Budget have increased tax rates on capital gains which impacts passive income taxation inside the corporation.

To make this comparison apples-to-apples, we’ll say that Andre invests into the same portfolio for all scenarios regardless of if it’s into the RRSP or if he invests inside his corp. It’s a balanced portfolio that earns 5% annually across all different income types like interest, dividends, capital gains, and deferred gains.

The final analysis will focus on the after-tax value of each option to Andre personally, as if he cashed out the RRSP and withdrew the funds from the corporation to use personally.

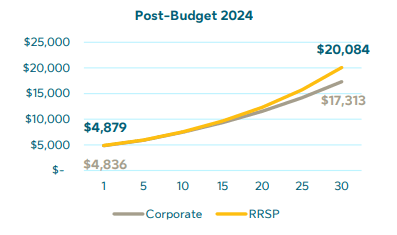

Here’s a graph that shows the growth over time for both scenarios – this shows what he gets to keep after paying taxes when he withdraws the investment personally. In the RRSP he takes it out of the RRSP and in his corporation he cashes in the investment and pays it out to himself personally as a salary from the corporation. You can see the growth visually in this graph. This is his RRSP growth vs if his corp pays the small business rate tax.

Post-Budget Graph

In the RRSP Scenario – the yellow line - If he invests and takes the money out and pays tax, he’s left with $4,879 in his jeans that he can spend If he invests through his corporation, pays the small business rate tax and then pays himself out as a salary he ends up with $4,836

You can see in Year 1: Both the RRSP and corporate investments start at approximately $4,879 (RRSP) and $4,836 (Corporate). This slight difference is due to the upfront taxation on corporate income, which reduces the amount available for investment.

Using British Columbia tax rates, by Year 11 the RRSP starts to outperform the corporate investment option. This is where the tax deferred growth inside the RRSP starts to shine. Every year after the corporate investment lags behind due to passive investment tax rates on interest, dividends, and capital gains.

If he cashes the RRSP out in year 30 he ends up with $20,084 after all taxes, while with the corporate investment option he ends up with $17,313 after paying it out to himself as a salary and paying all taxes. That gap shows the advantage of tax-sheltered compounding inside the RRSP, compared to getting taxed every year on investments held within Andre’s corporation.

It’s a full 13% better inside the RRSP when you cash it out in 30 years. We’re showing numbers here using a $10,000 investment, but this adds up to an extra $139,000 if you are starting with a million dollars instead of $10 grand. The RRSP consistently outpaces corporate investments over time, making it a better choice for business owners looking to maximize long-term growth.

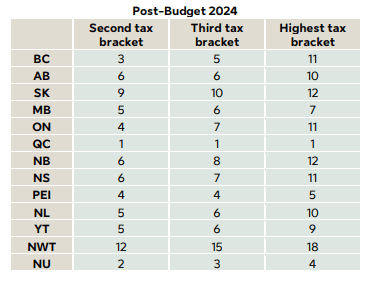

The graph on screen shows how many years it would take for the RRSP to become a better investment vehicle than your corp. This is by province - you can see that in BC the RRSP starts to beat the corporate investing after 11 years. In Alberta the RRSP wins after 10 years and in Ontario where we have a lot of clients the RRSP starts to win after 11 years same as BC.

If Your Corporation Pays Tax at the General Rate

Those numbers were all if your company pays taxes at the small business rate. When your company pays tax at the general corporate tax rate, the RRSPs tend to outperform more quickly. If your company pays at the general tax rate, the RRSPs begin to show a performance advantage within just one year for most provinces and territories.

Only British Columbia, New Brunswick, Yukon, and the Northwest Territories require more than a year at the top marginal tax bracket, with a maximum timeframe of 5 years. For most business owners paying the general tax rate, investing in an RRSP is the smarter choice for long-term financial growth.

If You’re in a Lower Tax Bracket When Withdrawing Funds

Your personal tax bracket will obviously fluctuate over your lifetime as you earn more and less. If you expect to be in a lower tax bracket when withdrawing funds than when you invested them, the time needed for the RRSP to outperform corporate investing decreases significantly.

The more tax brackets you drop, the faster the RRSP outpaces corporate investment returns, making RRSPs an even better choice for long-term savings. This is a pretty standard assumption when investing in an RRSP – that you will be making less income in retirement years, and you will be in a lower tax bracket. For a lot of people, it works like this.

Some people continue to make a high income even in retirement years. This would generally be a business owner or someone with a real estate portfolio that keeps paying rents or a big dividend portfolio that spits out dividends each month or quarter.

If You’re in a Higher Tax Bracket When Withdrawing Funds

Conversely some people’s tax brackets keep going up from when you deposit the investment to when you take it out. If you will make more money later, the time required for the RRSP to outperform corporate investments goes up.

However, even in these scenarios, the performance time shown for the "highest tax bracket" acts as an upper limit. With sufficient time, RRSPs still generally provide superior after-tax returns compared to retaining funds in your corporation.

Additional Factors to Consider

When deciding between RRSPs and corporate investments:

- What are your Investment Goals: Are you investing for the short term or long term?

- What is the Impact on Income-Tested Benefits like CPP and OAS: Grossed-up dividends from corporate funds can increase your net income, potentially reducing retirement benefits.

- Creditor Protection: RRSPs benefit from Federal bankruptcy protection and creditor protection in most provinces, while your corporate funds may remain exposed. There’s some legal protection to having funds inside your RRSP.

- Eligible Pension Income: RRSP withdrawals may qualify as pension income, while corporate funds are subject to TOSI tax on split income rules.

- Income Flexibility: RRSPs require mandatory withdrawals after age 71, while corporate funds offer more flexibility. This is a big one to consider so you don’t put “too much” money into your RRSP and it becomes trapped in there.

- Impact of Passive Income: Accumulating passive income in your corporation can lead to the loss of the small business tax rate. This is a big one that you need to consider in your calculations because it can cause a significantly higher tax bracket from the small business rate to the general rate for your company.

- Post-Mortem Planning. What happens when you die? Keeping the money inside your corporation increases complexity and costs for estate planning.

- RDTOH Considerations: You may need to recoup the Refundable Dividend Tax on Hand when retaining funds in your corporation.

Final Summary

Saving for your future income requires careful planning and an understanding of your options.

While RRSPs are specifically designed as long-term retirement vehicles, removing surplus money from your corporation to your RRSP often makes sense, especially under the new 2024 Federal Budget changes, which were designed to make corporate investing less attractive.

Ultimately, the decision depends on several factors, including corporate tax rates, personal tax rates (now and in the future), and the timing of withdrawals. And the answer this year might not be the same next year. Today it might make sense to put money in your RRSP and in a few years you keep more in the corp.

This is what a good financial advisor can help you figure out. This is what we do – we talk to clients now and also stay in contact throughout the year to keep updated and to adjust as needed.

If you're looking for someone to professionally manage your investment portfolio we are happy to talk and see if we can be a good fit to work together. We can help you with all types of accounts RESP, RRSP, TFSA, Non-registered, Corporate, CAD, USD.

Next Steps:

Since 2011 we have professionally managed 100s of Canadian families and business owner's investment portfolios. Our values are clear, we're Independent, we're Relationship Focused and we operate on a philosophy of No-pressure, No-rush.

With us you get a digital-first investment platform and a customized portfolio built and managed by a CFA Portfolio Manager.

Related Insights

Why Life Insurance Isn't Just for When You Die

If you think life insurance is something you'll never personally benefit from, you're missing the bigger picture. Permanent life insurance can provide liquidity, protect your...

Whole Life Insurance vs. Universal Life Insurance

Permanent life insurance can double as a powerful wealth-building tool—but not all policies are created equal. If you're an incorporated Canadian professional or business owner...

How Dollar‑Cost Averaging Is Helping Canadians Build Wealth

Between work, family, and everything else life throws at you—who has the bandwidth to watch the stock market every day? If you're a busy Canadian...

Must-Know Strategies for Business Owners Right Now

Over the past few weeks, our client meetings have shifted into a higher gear. The conversations we're having aren't about the basics anymore — they're ...

Using Life Insurance to Fund a Buy-Sell Agreement

Imagine one of your business partners passes away tomorrow. Suddenly, their spouse or their kids own a share of your company—and you're expected to buy...

5 Mistakes High-Income Canadians Make With Their Wealth Plans

If more money automatically meant more wealth, every top-earning Canadian would retire stress-free. But that's not reality. The gap between earning well and building lasting...

What are Notional Accounts and How do They Work in Canada

If you've wondered what are Notional Accounts and how do they work in Canada, this is the post for you. Most incorporated Canadians are great...

What Canadian Business Owners Are Telling Us Right Now — And What To Do About It

Every week, our advisors sit down with incorporated business owners and professionals across Canada. And while every client's situation is unique, the conversations we're having...

Retire Tax-Free in Canada Using the Insured Retirement Plan

What if your RRSP isn't enough to retire comfortably? And what if there was a way to access tax-free cash flow in retirement—without market volatility,...

How Canadian Real Estate Investors Are Using Whole Life Insurance

What if you could unlock hundreds of thousands in capital—without selling a single property or applying for another mortgage? In this article, we'll explore How...

Use Corporate-Owned Life Insurance to Transfer Wealth Tax-Free

What if your estate faced a $500,000 tax bill after you pass away—on capital gains alone? What if there was a way to fund that...

CDA: How to Pay Yourself Tax-Free from Your Corporation

Imagine extracting hundreds of thousands in corporate profits—tax-free—without triggering personal tax liability. That's exactly what the Capital Dividend Account (CDA) allows incorporated professionals to do...