Should you Invest using Dollar Cost Averaging (DCA) or a Lump Sum?

Curious about which investment strategy could maximize your earnings the most: dollar cost-averaging or a lump sum investment? Let's explore the numbers to uncover the pathway to greater financial growth.

So, what investment strategy is going to you the most money, dollar cost-averaging or a lump sum investment? I can’t see the future but based on data provided by the Royal Bank of Canada, we can look at the past 30 years and see what has the better track record.

Before we get into which is better, let’s define them.

What is Dollar-Cost Averaging?

Put simply, dollar-cost averaging, or DCA, is re-entering the market with a smaller sum regularly. This could be once a twice a month, once a week, or even every day, but it essentially means you invest something like twenty, fifty, or a hundred dollars as often as you can, to get as close to the average price of your investment as you can while spending a bit less at one time.

What is a lump sum investment?

A lump sum investment is well that, one lump sum, maybe you put it on around ten grand once a year and let that sit and grow until the next year when you put in another ten grand.

What the data says

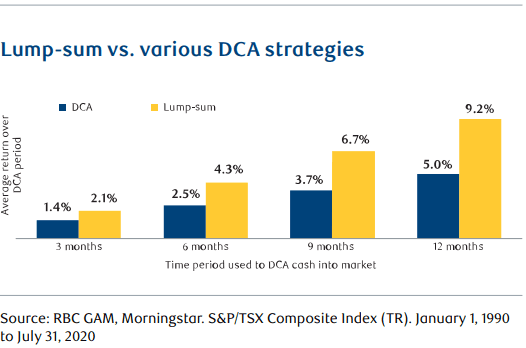

The data we have been provided with by RBC uses data going back thirty years that compares investing a lump sum against DCA strategies over periods of three months to twelve months.

The lump-sum strategy came out on top in each time-period. This is because markets generally rise over time. So, the DCA investor often bought in at higher average prices.

Things to keep in mind when looking at this, the results are based on a one-time, lump-sum investment of $10,000 made at the beginning of each time-period, and DCA installments of $10,000, spread out evenly each month over the course of each time-period.

Data is always very helpful when making investment decisions, but most of us don’t think like a computer or a calculator so our emotions also play a heavy role in our decisions, even when investing.

Imagine, the markets start to drop, how will you feel about investing a large lump-sum of cash? Will you worry that markets will plunge further – and delay investing? Worry can keep us on the sidelines – sometimes for a very long time.

Now, we have been provided with another chart, using data from the global financial crisis, which compares the experience of a DCA investor to a lump-sum investor. We look at two six-month periods: one where markets were falling and one where markets were rising.

Keep in mind for this chart, we make the following assumptions:

- Each investor has $50,000 in cash to invest

- The DCA investor deployed the cash across six equal monthly installments.

- The lump- sum investor deployed the entire sum of cash on the first day of the same six-month period.

Things to keep in mind.

During falling markets:

The dollar cost averaging (DCA) approach shielded the investor's holdings compared to the lump-sum investment. Not depicted in this chart: the DCA investor reached breakeven just three months after the market's low in June 2009. In contrast, the lump-sum investor did not surpass the initial portfolio value until December 2010.

During rising markets:

The lump-sum investor showed superior performance in the six months following the market low. Nevertheless, committing to a lump-sum investment during this period would have been highly unsettling, especially given the economic conditions at that time. Despite trailing the lump-sum strategy in terms of immediate results, the dollar cost averaging (DCA) investor still achieved commendable returns through a more cautious and gradual app

Final Notes

As we have discussed, the data demonstrates that lump-sum investing typically benefits investors. However, if re-entering or entering the market for the first time feels challenging, a dollar cost averaging (DCA) strategy can assist in taking that crucial initial step. Additionally, it offers a more consistent investment journey, which are essential factors in adhering to your long-term financial strategy.

Take Next Steps:

At Safe Pacific Financial, we help Canadian business owners, incorporated professionals, and investors structure their investment portfolios to achieve their lifestyle, retirement and legacy goals for their family.

To schedule a meeting time and see if we can be a right fit to work together, click on the button below.

Related Insights

You can now invest with us!

We have got a big update for you today – a brand new offering from us at Safe Pacific.

RRSPs for Canadian Business Owners, should you invest?

You have two main options: Today we’re going to go through these 2 scenarios – do you take your money out of the corporation and...

Why you Shouldn’t Withdraw Investments When Markets are Down

First of all, it's important to understand that markets are cyclical, so it’s natural for markets to go up and down. It’s part of how...

What type of Life Insurance can you use to Leverage and Invest?

Types of Life Insurance There are two major types of Life Insurance, Term, and Permanent Life Insurance. At Safe Pacific we set up both of...

How to Stack Investments with a Whole Life Policy in Canada

Watch this 3:23 mins Summary Video Because the cash values inside the policy are so stable, you can use the policy as collateral for loans...

The Canadian Business Owner’s Guide to RRSPs

Should you or shouldn’t you invest into your RRSP as a business owner in Canada. When you have your own business you have 2 main...

Everything you need to know about RRSPs, and more!

In this blog we will be covering the most common questions about the RRSP, to help you prepare for the rapidly approaching deadline. How does...

What's the difference between the TFSA tax free savings account and RRSP registered retirement savings plan?

(Scroll down for infographic) What's the difference between the tax free savings account and registered retirement savings plan? We show you the journey of putting...

Are TFSAs good for small business owners?

One of the main tax advantaged accounts you can use in Canada is the TFSA – Tax Free Savings Account. This is one of our...

Investments and Incorporation with Coal Harbour Law

What is Incorporation? Incorporating a company is creating a new stand alone legal entity that helps business owners shield themselves from personal liability. The process...

How Much Money Stays in Your Pocket? The Difference Between Interest, Dividends and Capital Gains Income

(Scroll down for full infographic)Usually our concept of income is derived from labor which leads to a fixed or variable wage for a certain time...

Financial Literacy Month - Talk to your children about Money

Did you know that 70% of wealthy families run out of money by their second generation? And if we go down to the third generation,...