Are TFSAs good for small business owners?

As a small business owner, what do you do when your corporation generates more income than you need for daily operations or personal expenses? The decision to save that surplus is crucial—should you keep it in the business or invest it personally? Let’s explore your options for securing a stronger financial future.

One of the main tax advantaged accounts you can use in Canada is the TFSA – Tax Free Savings Account. This is one of our favorite options for saving money and building wealth over the long term. We’re big fans.

We are going to go over how good TFSAs, or Tax-Free Savings Accounts are great for small business owners in Canada.

What is a TFSA?

I’ll make this part quick because we just posted a more comprehensive video about TFSAs that you can watch now, linked in the description and you can click somewhere on screen right now and watch it.

Introduced in 2009, the Tax-Free Savings Account (TFSA) allows Canadians aged 18 or older with a valid Social Insurance Number (SIN) to save and invest tax-free.

Contributions are not tax-deductible, but all income earned—whether from investments or capital gains—is tax-free, even when withdrawn.

Tax Benefits for Small Businesses in Canada: Understanding Corporate and Personal Tax Rates

Many small businesses in Canada benefit from favorable tax rates on active business income, commonly referred to as the "general rate." This combined federal and provincial general rate typically ranges between 23% to 31% across Canada.

If you’re a small business, you can also take advantage of the small business deduction on your net income up to $500,000 (the "small business rate")

The combined federal and provincial tax rate under the small business deduction is between 9% to 12% on the first $500,000 of income depending on your province.

Your personal tax is usually much higher than your corporate active tax rate. For ordinary income, the highest combined marginal personal tax rates can be more than 50%. Big daddy government is your partner in every dollar you earn and his goons at the CRA are out to collect.

It gets a bit more technical when it comes to paying yourself dividends and I’ll try to break it down in a simple way here.

For dividends, the highest combined rates are between 28% to 46% for eligible dividends and 37% to 49% for non-eligible dividends. The lower personal tax rates on dividends are because you’ve already paid corporate tax.

There are Eligible dividends based on the general tax rate, and non-eligible dividends based on the small business tax rate that you already paid in your corp.

Corporate vs. Personal Investment: Understanding Tax Deferral Opportunities

Unlike contributions to RRSPs, which benefit from upfront tax deferral, both TFSAs and corporate investments start with after-tax money. You don’t get any deductions upfront.

The difference is where the after-tax money originates.

For a TFSA, the funds are personal after-tax dollars, while corporate investments are made with after-tax corporate dollars. If your corporation’s tax rate is lower than your personal tax rate, you can benefit from a tax deferral advantage, as the corporation retains more after-tax money for investments.

When you invest corporately, you can grow your after-tax money with cheaper dollars, but you still can’t go out and buy a pair of shoes with that money. You still must get it out of your corporation if you’re going to spend it personally, and to do that you’re going to have to pay some sort of income tax. This is something you’ll work on with your accountant.

The potential tax deferral varies across Canada:

For corporate income taxed at the small business rate, the potential tax deferral ranges from 32.5% to 43.3%.

For corporate income taxed at the general rate, the deferral is approximately 17.5% to 27%.

To calculate your specific tax deferral, subtract your corporation’s tax rate from your current personal tax rate.

Here are some Key Considerations for Maximizing Tax Deferral in Corporate Investments

A lower tax rate within the corporation doesn’t automatically guarantee a tax deferral advantage. The goal is to maximize after-tax personal income when you cash out the investment and put the money in your pocket. Like investing in RRSPs, several factors influence the outcome, including:

- Your corporation’s initial tax rate on active business income, whether taxed at the general rate or small business rate.

- Your personal tax bracket at the time of investment versus when you liquidate the investment.

- The form of investment income generated, such as interest, dividends, capital gains, or deferred gains.

- The time horizon or duration for which the funds are invested.

These are all things to think about when you’re trying to optimize your wealth building. You must be strategic when you pull income, where you invest and what you invest in. Again, working with a good financial advisor (like us) and your accountant on a regular basis can help you decide how to invest and when.

Investment vehicle characteristics

When comparing investment options between Tax-Free Savings Accounts (TFSAs) and corporate investments, there are key differences in tax implications and growth potential.

For business owners deciding whether to invest within a TFSA or retain funds inside their corporation, understanding the tax landscape is crucial.

For TFSAs, contributions come from after-tax personal income, meaning that you pay personal tax at your regular tax bracket when withdrawing funds from the corporation to invest in your TFSA.

Once the money is invested in a TFSA, however, growth is tax-free. This means there are no additional taxes on interest, dividends, or capital gains generated by the investment.

Furthermore, withdrawals from a TFSA are also completely tax-free, making it an attractive option for personal wealth accumulation.

In contrast, corporate investments are subject to corporate tax at either the general or small business rate, depending on the corporation’s total income.

When investments are made within the corporation, growth is taxable depending on the type of passive investment income. Interest is taxed at 46% - 54% when you invest in your corp. If you’ve invested in a Canadian company and it pays dividends, that’s taxed at 38%. And now capital gains are taxed higher because the inclusion rate has gone up to 66%.

So, when you’re investing inside your corporation there’s the initial advantage of a lower corporate income tax rate before you invest the money. But then when you invest in your company there are no tax benefits on the investment.

There are passive investment tax credits such as the Refundable Dividend Tax on Hand (RDTOH) that can help recoup some of the taxes paid when dividends are distributed to shareholders.

While TFSAs provide tax-free growth and withdrawals, corporate investments offer potential tax deferral advantages. When funds are eventually distributed from the corporation, they may be subject to capital gains tax or dividend tax, depending on how they are structured.

Business owners must weigh the benefits of the tax-free growth in a TFSA against the corporate tax deferral to determine which investment vehicle will yield better after-tax returns when funds are liquidated and distributed.

TFSA vs. Corporate Investments: Which Option is Best for You?

We’ll look at Andre's financial situation provided in the article. Andre, a resident of Ontario, has maximized his RRSP contributions and is now in the highest tax bracket. His corporation, also based in Ontario, has a $10,000 pre-tax surplus available for investment.

Here’s what happens if he pays himself the money and invests in his TFSA

If Andre’s corporation pays him a salary, it deducts the $10,000 from the company’s pre-tax profits, reducing the corporation’s taxable income to zero. Andre then receives the $10,000 and is subject to a personal income tax rate of 53.53%, leaving him with $4,647 to invest in his TFSA.

Here’s what happens if he keeps the money in the corp and invests it there

Alternatively, if the corporation retains the surplus, the after-tax amount available for investment depends on the corporation’s tax rate:

- Small Business Rate: With a 12.2% corporate tax rate, the corporation would retain $8,780 to invest.

- General Rate: At the general corporate tax rate of 26.5%, the company would retain $7,350 to invest.

The corporation then invests this after-tax amount, and the corporate investment income is subject to corporate tax rates on interest, dividends, and capital gains, as outlined in the earlier section. Note that the federal government recently increased the capital gains inclusion rate which will impact the passive income tax on corporate investments.

Here’s the analysis – is it better for Andre to pay himself the money and invest in his TFSA or to keep the money in the corporation and invest it there?

To make a fair comparison, let’s say that in both scenarios Andre invests the after-tax amount into the same balanced portfolio and gets a 5% annual return divided between interest, dividends, capital gains, and deferred gains.

To assess the true benefit, we’ll evaluate the after-tax value of both options once the funds are withdrawn, either from the TFSA or the corporation. This analysis will help determine the best strategy for Andre’s long-term financial goals based on current and proposed tax changes.

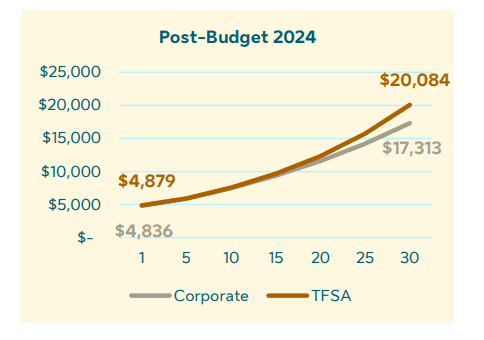

The article provides a wonderful graph, we’ll put it here so that you can visualize what we’re going over here.

When a corporation pays tax at the small business rate, the TFSA begins to outperform the corporate investment immediately.

Since the capital gains inclusion changes in the 2024 budget, the initial amount available from the corporation is lower, both at the start and in the long term, due to increased taxes on corporate realized capital gains.

While the TFSA outperforms early on, it takes time for the difference in growth to exceed 1%.

It’s important to note that the lower the interest income generated inside your corporation, the better the corporate investment performs. However, it’s crucial that your investment strategy aligns with your risk tolerance.

We don’t recommend selecting investments outside your comfort zone purely to achieve better tax results. For instance, corporate class mutual funds can reduce interest-generating investments, but returns on these investments can vary.

It’s essential to consult with a financial advisor to ensure your investments match both your risk tolerance and long-term financial goals.

The new capital gains inclusion rate has significantly impacted corporate investments, particularly with the increased tax on capital gains. Investing in a TFSA was better before, but now it’s even better than before.

This analysis also changes depending on your province

The performance of TFSA vs. corporate investments varies depending on tax rates across different provinces. In each case, we are analyzing how long it takes for the TFSA to outperform corporate investments by at least 1%.

Understanding how these tax changes will affect your investment strategy is critical for maximizing long-term gains.

For tailored investment strategies and to understand how these changes affect your financial situation, talk to us or to your financial advisor and we can help guide you and make sure you know all the details.

TFSA vs. Corporate Investment: Time Needed to Outperform by 1% Based on Your Tax Bracket

Here’s a summary of how long it takes for a Tax-Free Savings Account (TFSA) to outperform a corporate investment by 1%, assuming you remain in the same tax bracket throughout your lifetime.

The analysis covers three key tax brackets:

- Second federal tax bracket (approximately $56,000 annual income)

- Third federal tax bracket (approximately $112,000 annual income)

- Highest federal tax bracket (approximately $246,000+ annual income)

When your corporation pays tax at small business rates, a TFSA typically starts providing more after-tax returns from the beginning.

Since the 2024 Federal Budget made changes to the capital gains inclusion, the time needed for a TFSA to beat corporate investments by more than 1% is much quicker due to increased taxation on corporate capital gains. Yay more taxes!

You can see here a visual representation of how many years for each tax bracket in each province for pre and post budget changes in this graphic below.

Comparing TFSA to RRSP Investments

How does this compare to RRSP investments? Interestingly, the timeline for a TFSA to outperform corporate investments mirrors the timeframe seen in RRSP analysis. If you remain in the same tax bracket throughout your lifetime, the after-tax returns from both TFSA and RRSP investments will be identical once liquidated. This is because both RRSPs and TFSAs grow tax-free and maintaining a consistent tax rate means neither will have an advantage over the other in the long term.

Understanding how TFSAs, corporate investments, and RRSPs perform in relation to your tax bracket is critical for optimizing your investment strategy and achieving the best after-tax returns.

Impact of Changing Tax Brackets When Removing Funds

If you're in a lower tax bracket when withdrawing funds, like in the RRSP analysis, this can impact your investment outcomes. Should you move to a lower tax bracket between the time of investing and liquidation, it takes longer for the TFSA to outperform corporate investments. In this scenario, the corporate tax deferral becomes more beneficial because you initially withdraw corporate funds at a higher tax rate and reinvest in a TFSA, but later remove funds from the corporation at a lower rate.

For corporations paying tax at the small business rate, the TFSA often takes a considerable amount of time to outperform corporate investments, sometimes taking 18 to 30+ years across Canada to see more than a 1% outperformance. This is due to the larger corporate tax deferral at small business rates. The more tax brackets you drop upon liquidation, the longer it takes for the TFSA to catch up.

At the general tax rate, the TFSA outperforms corporate investments more quickly, as the tax deferral advantage is smaller. However, it can still take 10+ years for the TFSA to outperform by more than 1%. Again, dropping multiple tax brackets when withdrawing the funds extends the time it takes for the TFSA to show greater returns.

TFSA Outperformance in a Higher Tax Bracket

If you move to a higher tax bracket when withdrawing funds, the tax-free growth of the TFSA becomes even more significant. In this case, you initially withdraw funds from your corporation at a lower tax rate and invest in a TFSA, which grows tax-free. Later, you withdraw corporate investments at a higher tax rate, making the TFSA a more favorable option. Regardless of whether your corporation pays the small business rate or general rate, the TFSA outperforms from the start and continues to offer a significant advantage.

Additional Considerations

There are several factors to consider when deciding between corporate investments and a TFSA:

TFSA contribution limits: TFSAs have a "use it or lose it" rule, meaning you cannot contribute after death, and your estate cannot make contributions like spousal RRSPs. Any unused contribution room is lost upon death.

Investment goals: TFSAs can be used for both short-term and long-term goals, whereas RRSPs are primarily for retirement. Your goal and timeline will influence your decision.

Impact on income-tested benefits: Withdrawals from a TFSA don’t affect income-tested benefits, whereas corporate dividends may.

Income splitting: Be aware of income-splitting rules, which could influence your decision if corporate funds are involved.

Passive income accumulation: If your corporation is accumulating passive income, you may lose access to the lower small business rate.

Post-mortem planning: Keeping funds in your corporation could complicate estate planning and increase costs.

Recouping RDTOH: You'll need to plan to recover your refundable dividend tax on hand (RDTOH) if funds are kept within the corporation.

Summary: TFSA vs. Corporate Investment for Canadian Business Owners

For most business owners, using a TFSA for future savings makes sense, especially given the proposed 2024 Federal Budget changes, which increase capital gains inclusion rates for corporate investments.

However, the decision isn’t always straightforward. The time it takes for a TFSA to outperform corporate investments depends on several factors, including your current and future tax brackets, corporate tax rates, and when you plan to access the funds. Use this information as a guideline to make the best decision based on your financial goals and circumstances.

Today’s video was a bit more technical than our regular ones. If you’ve got any questions, please reach out – I love to talk about this stuff and I can talk about it all day if you let me.

If you’ve got money in your corp. and are wondering what the best way to invest and grow it is, contact us and we can help you. Our team is good at this, and we can put you in the right types of accounts so that you can reach your financial goals in a quicker and smoother way – while also not distracting you from your number one wealth generator – which is your business.

Next Steps:

We have helped 100s of Canadian business owners and high-income professionals build and manage their TFSA investment accounts since 2011.

To see if we can be a good fit to work with you, schedule a no-pressure Discovery call with one of our advisors today.

Related Investment Articles

Are TFSAs for Canadian Business Owners a good choice?

We have been given a detailed article courtesy of CIBC who has done all the math for us, and we will be using that today...

What's the difference between the TFSA tax free savings account and RRSP registered retirement savings plan?

(Scroll down for infographic) What's the difference between the tax free savings account and registered retirement savings plan? We show you the journey of putting...

RRSPs for Canadian Business Owners, should you invest?

You have two main options: Today we’re going to go through these 2 scenarios – do you take your money out of the corporation and...

The Canadian Business Owner’s Guide to RRSPs

Should you or shouldn’t you invest into your RRSP as a business owner in Canada. When you have your own business you have 2 main...

Everything you need to know about RRSPs, and more!

In this blog we will be covering the most common questions about the RRSP, to help you prepare for the rapidly approaching deadline. How does...

Should you Invest using Dollar Cost Averaging (DCA) or a Lump Sum?

So, what investment strategy is going to you the most money, dollar cost-averaging or a lump sum investment? I can’t see the future but based...

You can now invest with us!

We have got a big update for you today – a brand new offering from us at Safe Pacific.

Why you Shouldn’t Withdraw Investments When Markets are Down

First of all, it's important to understand that markets are cyclical, so it’s natural for markets to go up and down. It’s part of how...

How to use Life Insurance as an Investment in Canada

Often when people think about life insurance they think of it as an expense, or a drain on their income. Today we’re going to be...

Investments and Incorporation with Coal Harbour Law

What is Incorporation? Incorporating a company is creating a new stand alone legal entity that helps business owners shield themselves from personal liability. The process...

How to Stack Investments with a Whole Life Policy in Canada

Watch this 3:23 mins Summary Video Because the cash values inside the policy are so stable, you can use the policy as collateral for loans...