What is The Insured Retirement Plan?

Today we are going over the Insured Retirement Plan or IRP. This is a plan that can unlock financial freedom today while you’re working, tomorrow when you want to retire and at the end when you want to leave a legacy for your family. This is a quick guide for Canadian business owners that you probably won’t find anywhere else.

The Insured Retirement Plan is an ideal follow-up strategy for the IFA Immediate Financing Arrangement strategy. You can see our other multiple videos on YouTube about the IFA strategy.

So, what are we going over today?

We will start with who it is for, how it works and then talk about some of the benefits of this type of strategy.

We’ll show you a sample illustration with real numbers and then we’ll talk about some risks and pitfalls you need to avoid if this is a strategy you’re trying to do for yourself.

Who is it for?

So, you are a high-income earner and in good health with a need for permanent life insurance. You have maximized retirement contributions and have significant assets in taxable investments. You want to access some of the money to supplement your retirement income but still protect the estate value available to your family or other beneficiaries after your death.

If you sell or reallocate assets, it can trigger capital gains and you’ll reduce your after-tax income and the value of your estate.

The Individual Retirement Strategy offers advantages that can protect the value of your estate while achieving your retirement goals.

You’ll need to set this up at least 5 – 10 years before your want to “retire” so it gives the plan some time to get loaded up. You must make the contributions into the plan before you can use it.

How it Works

You purchase a permanent life insurance policy – a participating whole life policy from one of Canada’s major life insurance companies.

Growth within the policy can accumulate on a tax-preferred basis and when additional retirement income is needed, you can pledge the cash values in your policy as collateral for a series of tax-free loans from a third-party lender like a bank.

On death, the tax-free death benefit pays the outstanding loan plus accumulated interest and any remaining death benefit is paid tax free to your beneficiaries.

The Benefits

Tax preferred asset growth

There is no tax payable on the growth of the policy’s cash value if it remains within the policy and the policy is funded within the CRA’s allowable limits called MTAR in Canada. This helps reduce taxable income and can result in greater asset growth.

Tax savings through the collateral assignment of your policy to a bank

When additional retirement income or cash access is needed, it may be attained by accessing the accumulated value of the life insurance policy through a series of collateral loans against the life insurance policy. Currently, the Income Tax Act of Canada does not treat collateral loan proceeds as income, so this amount is potentially tax free to you. This may help to reduce income taxes when accessing cash during your lifetime.

Alternative Income Options

The Individual Retirement Strategy illustrates the benefits of using a collateral loan to attain supplementary income; however, there are alternative ways to access the accumulated cash value of the life insurance policy. You may have the ability to access cash value directly through a policy loan or withdrawal, though these options can change the taxability of your plan.

Tax deductibility through collateral assignment

When collateral loan proceeds are being used to earn income from a business or property, interest on the loan may be tax deductible. Additionally, when the policy is used to secure the collateral loan, some or all of life insurance premiums may also be deductible. The resulting savings allow you to access cash in a tax-efficient manner.

The death benefit pays out tax free and privately to your beneficiaries

When you pass away, your beneficiaries receive the death benefit tax free. By avoiding settlement costs, a larger after-tax amount can be paid to your beneficiaries when compared to taxable investments.

Some numbers

For quick heuristics or rule-of-thumb numbers your minimum budget should be an annual deposit of $50 thousand or more for at least the next 10 years. Ideally it would be $100 thousand or more for 10 years because that opens the lending options and gives you access to more banks and more services.

We often work backwards with clients from their desired annual cashflow in retirement. For example, if you want to retire with an additional $100 thousand per year after tax, I can work backwards and tell you how much to deposit each year.

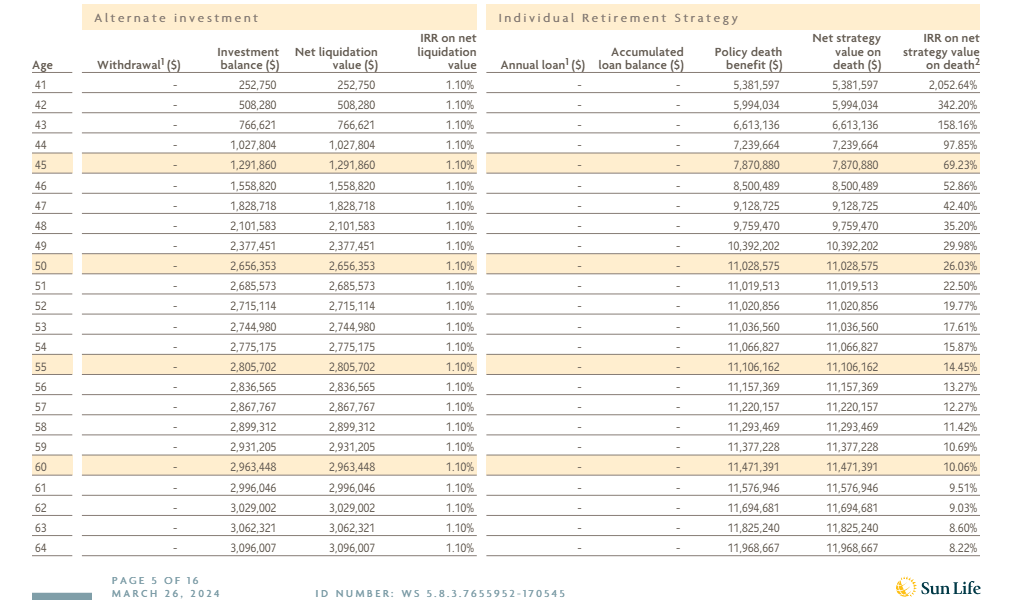

Now, I’m going to show you some illustration numbers that I ran with Sun Life. This is for a 40-year-old who will be saving $250,000 into this plan for 10 years until he’s 50 and then will start taking retirement income at your standard retirement age 65 until he passes away at 90.

You will see in this scenario that John Smith puts in his $250 thousand in year 1 and gets about $5.3 million in life insurance that will grow over time.

After 10 years when he’s 50 he will have deposited $2.5 million and has over $3 million in cash values and $11 million in life insurance death benefit. After year 10 he never puts in another dollar into this plan, but the cash values and the death benefit continue to grow.

Now he wants to retire at 65 and he has over $6 million in cash values and $12 million in death benefit. This was growing for him the whole time without him having to do anything.

So, he takes his policy to the bank and sets up retirement funding loans. In this scenario, he can get $332,983 tax-free every year for the rest of his life. You can see this in the Annual Loan values column.

Then, when he passes away at age 90, he will have borrowed $17 million from the bank to fund his retirement. That will get paid off from his life insurance proceeds of almost $22 million dollars which you can see in the Policy Death Benefit column. The remainder $4.8 million, can be paid out to his beneficiaries quickly, privately and tax free.

So what happened here?

He funded his retirement for 10 years

He took tax free retirement income for 25 years

And when he passed away, $4.8 million was paid out to his kids or charity or whoever he set up as his beneficiaries.

This sounds great, but there are risks to this strategy like with any other financial strategy.

At Safe Pacific we are straight up so we are not going to dance around the risks.

First, this strategy involves the maximum funding of a life insurance policy. Some people don’t like life insurance and don’t want life insurance, so this is obviously not a good idea for you if you don’t want or need the life insurance in the first place. And I'm not going to waste your time or my time trying to convince you that life insurance is a good idea.

We’ve had it where someone wanted to get all the tax and leverage benefits of this strategy but was trying to figure out all sorts of ways to get rid of the life insurance part - but that doesn’t work because the life insurance is the underlying core to everything.

Like I mentioned above, the budget for something like this would be a 5 or 6 figure annual premium deposit for 10 years or more. So, if this doesn’t sound like something you can get behind, then this probably isn’t for you.

Taxes could change.

Currently, the Income Tax Act of Canada does not treat collateral loan proceeds as income, so these amounts are potentially tax free. Tax laws are subject to change and the tax treatment of loans, interest deductibility, and life insurance policies may change between now and the time you want to retire and there might not be any grandfathering provision.

You might not be able to get a loan in the future

Your ability to access the cash value of the policy in the future through a collateral loan is not guaranteed. It will depend on your ability to qualify for the loan and the lender’s willingness to issue the loan.

When you start taking income you’re locking in

When you’re funding this plan, you have a lot of options and flexibility with what you do with the insurance policy and values. But when you want to start the retirement income part of the plan a lot of that flexibility goes away.

Once a policy has been collaterally assigned, you cannot withdraw funds, take a policy loan, or make changes to the policy without either first receiving the lender’s consent or paying off the loan balance.

You might need to put up additional collateral to get the loans in the future

The maximum amount you can borrow without requiring additional collateral is limited by the lender. It will be a certain percentage of the policy cash value. If the policy doesn’t perform the way we illustrate it, that will impact how much lending you can access and if you need to put up additional collateral.

There’s interest rate risk

The interest rate that you will pay on the loan is not guaranteed and can fluctuate. Higher than expected interest rates may cause the loan to policy cash value percentage to exceed the maximum collateral percentage. The bank might ask you for additional collateral or adjust the amount they’re going to lend you.

Often, we introduce a concept or strategy like this to someone and they are not ready for it now... they are still building and, on a trajectory, and then in a couple of years when they’re ready they reach out. In fact, many of our best clients happened just like that - not ready now but will come back in a couple of years and knock it out. But you really should know something like this exists now.

In Conclusion

The Insured Retirement Plan or IRP is a great financial strategy for the right type of person with the right type of cash flow, wealth or retained earnings in the holding company.

To schedule a call with one of our advisors and see if this strategy could work for you, please click on the button below. We operate with a philosophy of No-pressure, No-rush so you can feel comfortable working with our team.

Next Steps

At Safe Pacific Financial, we specialize in helping Canadian business owners, incorporated professionals, and investors build an Insured Retirement Plan using properly structured whole life insurance.

This gives them maximum wealth protection, tax savings and a guaranteed legacy for their families.

Related Insights

All About the Insured Retirement IRP Strategy in Canada

What is an Insured Retirement Plan or IRP?

We’re going to cover: What is an IRP or Insured Retirement Plan? An IRP is a strategy that uses insurance and leverage to supplement Canadian’s...

The Ten Commandments of Whole Life Insurance in Canada

Today's blog post is a reaction to this great article titled “The Ten Commandments of Whole Life Insurance”. Something that we like about this article...

Life Insurance: Should you get it if you’re retired?

“People often say, ‘The kids are out of the house. I no longer have a mortgage, and so why would I pay a premium for...

The Advantages of Whole Life Insurance for Retirement Planning

Here’s the quick version of how it works and then we’ll get into more detail. You start by over funding a participating whole life insurance...

What's the difference between the TFSA tax free savings account and RRSP registered retirement savings plan?

(Scroll down for infographic) What's the difference between the tax free savings account and registered retirement savings plan? We show you the journey of putting...

Why you Shouldn’t Withdraw Investments When Markets are Down

First of all, it's important to understand that markets are cyclical, so it’s natural for markets to go up and down. It’s part of how...

You can now invest with us!

We have got a big update for you today – a brand new offering from us at Safe Pacific.

How to use your Life Insurance Policy to Invest

The five questions we are going to be answering in this blog are: What kind of Insurance Policy can you do this with? We often...

How to Stack Investments with a Whole Life Policy in Canada

Watch this 3:23 mins Summary Video Because the cash values inside the policy are so stable, you can use the policy as collateral for loans...